I traveled via international airports in the time of coronavirus and discovered that face-mask fashion is a thing. Twenty-something partiers on their way to the Berlin nightclubs wore baby-blue paper surgical masks haphazardly. A pair of teen siblings donned matching red masks, while their parents went mask-less. And, my personal favorite: a tall woman, accessorized with randomly placed strips of fake fur, and who was clearly fresh from a visit to Dr. E, Bulgaria’s most famous cosmetic surgeon. Her black pleather face mask matched her form-fitting pants to a tee.

Hopefully this style trend will keep the virus, which has now killed more people than SARS, from spreading. But all the face masks in the world won’t stem the economic malaise, which has already infected energy markets and may soon reach into the oil patches of the United States, for better and for worse. It’s a real-time demonstration of the fragility, and far-reaching nature, of the global economy, as well as a repudiation of specious claims that the US is energy independent.

The first fatality from the virus — officially known as 2019-nCov — was reported on Jan. 11. Within a week, cases were confirmed in the US, France, Nepal, South Korea, and other nations. And on Jan. 22, travel restrictions were put in place in parts of China and factories and other businesses, including Disneyland Shanghai, started shutting down. Many flights into and out of China were cancelled. And the nation’s giant economy started slowing down.

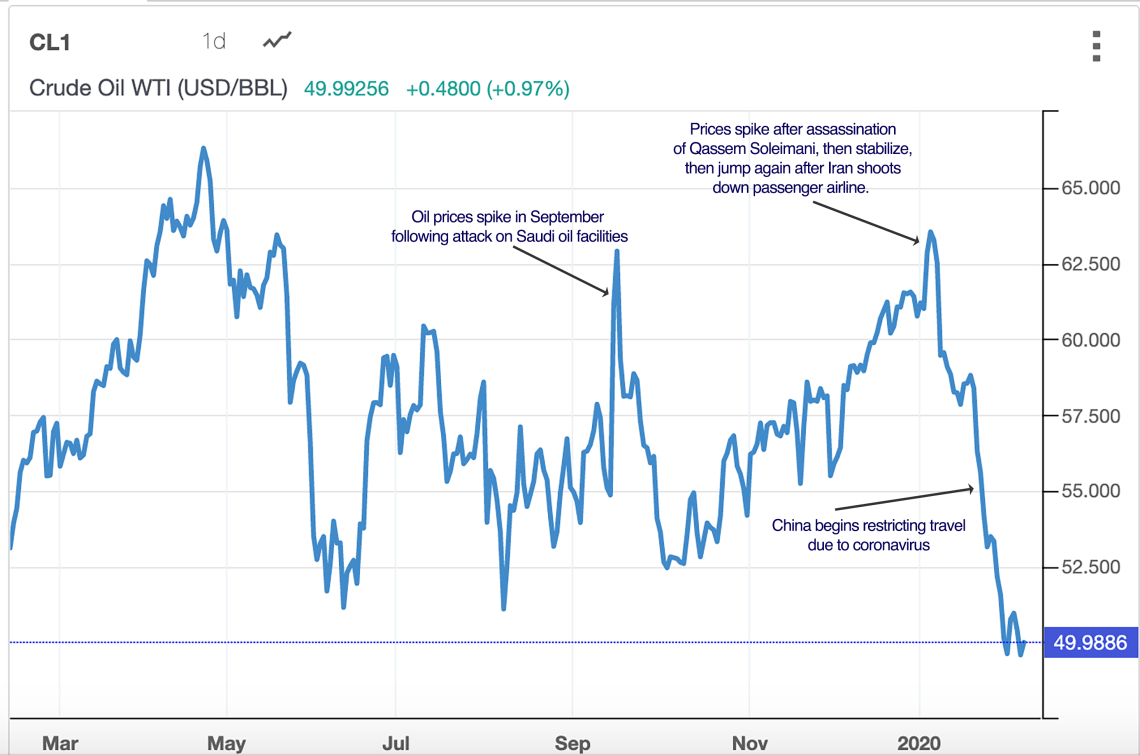

Oil prices, which had been elevated in part due to fears that Iran would retaliate for the assassination of Qassem Soleimani by attacking an oil-producing neighbor or shutting down the Strait of Hormuz, dropped precipitously. China is the world’s second biggest consumer of petroleum, after the United States. So if the nation suddenly pauses its gluttony, even just a little bit, it can ripple throughout global energy markets (I expand on this in the upcoming issue of High Country News).

Which is exactly what is happening. Thanks to the coronavirus, China has slowed its petroleum intake by an estimated 2 million to 3 million barrels per day — a massive hit to the global market. And when demand drops and supply* doesn’t, prices fall. On Feb. 10, the West Texas Intermediate price — the US benchmark — fell below $50 per barrel for the first time in over a year.

A decade or so ago, this would have been nothing but good news for the US economy, and for President Donald J. Trump. That’s because the US was primarily an oil consumer, and low oil prices lead to low gasoline prices, meaning folks can spend money on something other than filling their tank, thus fueling the economy. As Trump is prone to do, he’d then take credit for the economic surge, even though it was triggered not by his policies, but by the side-effects of a deadly virus.

The US continues to be the world’s greediest gas glutton. However, over the last decade, it has also become one of the world’s largest oil producers, and recently became a net exporter of petroleum products. That means low oil prices will also sting the economy, particularly in the booming oil patches, be they in New Mexico, Texas, Colorado, or Wyoming. And that will reverberate back through the national economy as a whole, which has been boosted significantly by the drilling boom.

Take New Mexico, where a drilling frenzy is turning the southeastern corner of the state into both a cash cow for the state, and an environmental and human health disaster for the people living there. In November, New Mexico produced nearly 32 million barrels of oil, about 500 times its monthly production in 2009. That brought in some $3.1 billion in royalties and tax revenue to the State of New Mexico last year.

Most of that revenue is based on the gross value of the oil and gas produced, which means that state revenue will decrease alongside the price of oil, the amount depending on how much production climbs or falls. If the WTI drops by ten percent over the year, then New Mexico could expect to pull in some $300 million less in 2020, assuming production holds steady.

Some analysts predict that ripple effects of the coronavirus could push oil prices down to $40 or even $30 per barrel, which would represent nearly a 50 percent decrease from the 2019 average price. If that happens, and if those low prices hold for a significant amount of time, then drilling will slow down, the boom will bust, and thousands will lose their jobs, as was the case after oil prices crashed in 2014. A drilling slowdown will eventually lead to a drop in production, which will deal another blow to state coffers.

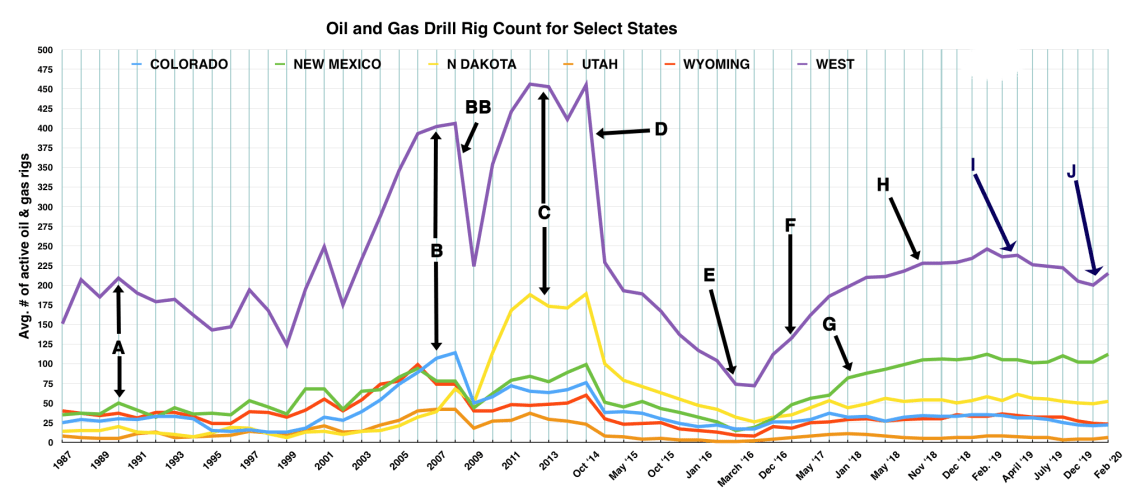

BB. The drilling and fracking boom resulted in a glut of natural gas flooding the markets, which combined with the global economic crisis to cause both oil and natural gas prices to crash. The big losers were natural gas producers in the West, who saw Eastern markets get taken over by producers in the Marcellus Shale formation in Ohio and Pennsylvania. C. While natural gas prices failed to rebound, oil prices jumped right back up, buoyed by growing demand from Asia. Meanwhile, in response to the financial crisis, the Federal Reserve encouraged high-risk, high-return investment — in drilling, for example — with quantitative easing and near-zero interest rates. That brought the debt-fueled drill rigs back to the West to go after plays that previously had been inaccessible. Geographically, however, the boom was shuffled dramatically. This time, North Dakota — which had mostly been left out of past booms — became the hottest oil patch in the nation. Wyoming and Colorado, meanwhile, were left with only about half as many operating rigs as they’d seen during the natural gas boom. D. Burgeoning supply from U.S. shale plays collided with waning demand from China and other global consumers. Meanwhile, Saudia Arabia and OPEC, breaking from past practice, kept on pumping oil out in high volumes, causing oil prices to plummet from a record high in summer of 2014 to near record lows just months later. Drilling rigs were packed up and put in storage, and nearly 55,000 people lost their jobs in the oil and gas extraction sub-sector. E. Global oil prices bottomed out in early 2016, and slowly began to reverse course as soon as Saudi Arabia announced a ceasefire in the price war against U.S. shale producers, meaning it would cut production. F. Trump took office in January 2017, months after oil prices — and rig counts — had begun their rebound. He immediately began attempts to roll back regulations, and also gave the Dakota Access Pipeline the go-ahead, which purportedly would result in a return of the North Dakota boom-times. G. While oil prices have gone up, they have only gone up enough to make new drilling projects in some areas profitable. That has favored producers in the Permian Basin of New Mexico and Texas where costs are lower, in part because they are closer to the Gulf Coast refineries that purchase their crude. Meanwhile, North Dakota, once the nation’s drilling hotspot, lags behind, even with crude flowing through the Dakota Access Pipeline. Employment in oil and gas extraction is up only about 8,000, or about five percent, from its lowest point in 2017. This has everything to do with prices and very little to do with policy. H. The rig-count rebound ebbed as oil prices drop again — a possible sign of a cooling global economy. I. Despite rolling back dozens of regulations, reducing national monuments to make way for extractive industries, and putting up millions of acres of land for lease, Trump has failed to spark a drilling boom like the one that occurred from 2010-14. That’s because the boom is fueled by high prices, debt, and technology. Easing regulations only serves to increase corporate profits. J. Prices climbed in late 2019 and early 2020 due to attacks on Saudi oil facilities and fears of Iranian retaliation for the killing of Qassem Soleimani. The coronavirus-related price crash won’t show up in rig counts for months — and that’s only if low prices hold.

And yet, amidst all the doom and gloom surrounding the coronavirus, there is one bright note: Global carbon emissions will dip, at least slightly, as a result of all of this. By reducing its consumption by 2 million to 3 million barrels of oil per day, China is keeping about 1.08 million tons of carbon dioxide out of the air each day. And that’s just from consumption of that oil; the extraction, transportation, and refining of each barrel of oil also results in substantial emissions of methane, carbon dioxide, and other greenhouse gases. If low oil prices stick, and a drilling slowdown results, then the climate benefits will be even greater**.

Air travel in and out of China has also dipped tremendously, and aviation is a major contributor of greenhouse gas emissions. A single person flying economy class from Los Angeles to Beijing and back contributes about 3.6 tons of carbon dioxide emissions. As is often the case, the wealthy have a bigger impact, with business class passengers contributing more than 10 tons each, and first class folks more than 14 tons. (And, yes, I was in an international airport to fly somewhere, and yes I’m a hypocrite, but at least I always fly economy — not that I have a choice). More than 1 million “weekly scheduled seats” have been cancelled, which adds up to a lot of carbon that’s staying out of the atmosphere***.

In other words, by taking measures to avoid a human-health disaster, government officials and corporations are inadvertently cutting global greenhouse gas emissions. It’s too bad they can’t manage to do the same, intentionally, in order to avert a planetary climate catastrophe.

*OPEC has cut oil production in recent months to buoy global prices, and they’ve extended the cuts due to the coronavirus. However, thus far the cuts only amount to about 600,000 barrels per day, meaning that it won’t get close to offsetting the reduction in demand from China.

** Some of this may be offset by an increase in gasoline consumption in the US due to lower prices at the pump. But various studies have shown that gasoline demand is not all that price elastic. That is, demand doesn’t change significantly due to price fluctuations. That said, the issue of gasoline elasticity is up for debate.

*** Some of this is may be accounted for in the reduction in demand for petroleum as a whole.

###